Beginner’s Guide to Zero-Based Budgeting: How to Give Every Dollar a Purpose

- MTK Marketing LLC

- Sep 6

- 6 min read

Disclosure: I may earn a small commission for purchases made through affiliate links in this post at no extra cost to you. I only recommend products I truly believe in. Thank you for supporting my site!

Do you ever get to the end of the month, look at your bank account, and think, "Where did all my money go?" You know you got paid, you paid your bills, but the rest seems to have vanished into thin air. You’re not alone.

This feeling of having money but nothing to show for it is one of the most common and frustrating financial experiences.

The problem isn’t that you don’t make enough money; it’s that your money doesn’t have a plan. Without a plan, your dollars will wander off without your permission, spent on impulse buys, forgotten subscriptions, and things that don’t align with your real goals.

This is where zero-based budgeting (ZBB) comes in. It’s not just a budgeting method; it’s a philosophy of intentionality with your money.

Made famous by personal finance expert Dave Ramsey, this method is the key to going from wondering where your money went to telling it exactly where to go.

This beginner’s guide will walk you through everything you need to know: what zero-based budgeting is, why it’s so effective, and exactly how to create your first budget. By the end, you’ll be equipped to give every single dollar a purpose and build a life of financial clarity and control.

What is Zero-Based Budgeting? (It’s Not What You Think)

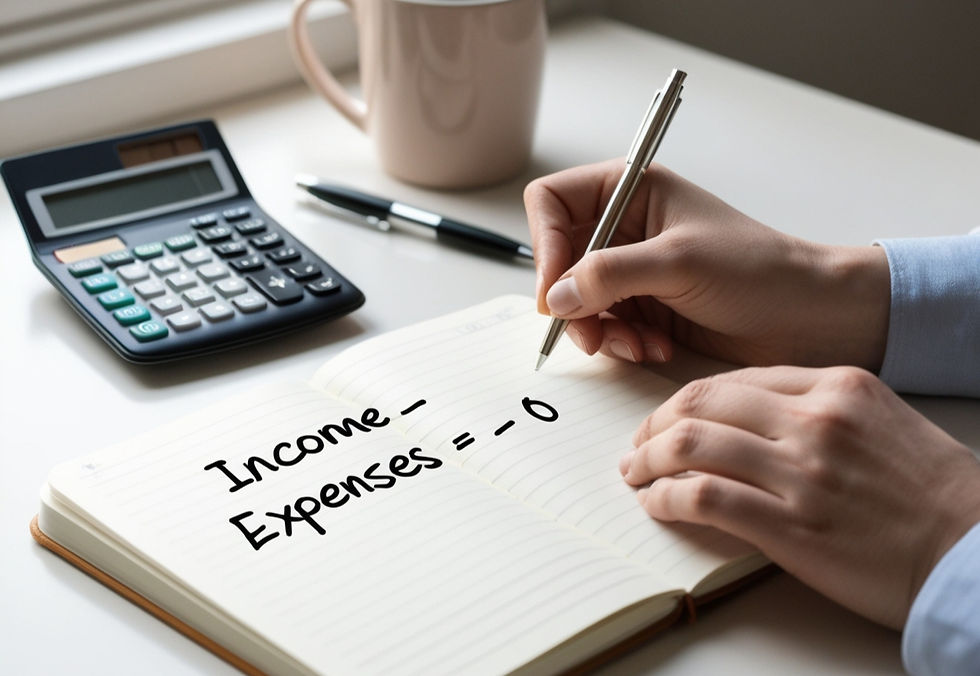

The core principle of a zero-based budget is simple:

Your Income – Your Expenses = $0

This equation often causes a moment of panic. "Zero? You want me to have zero dollars at the end of the month? That sounds terrible!"

But that’s not what it means. A zero-based budget does not mean you have zero money in your bank account. It means that every dollar you earn has been assigned a specific "job" before the month begins. Those jobs can be:

Expenses: Rent, groceries, utilities, gas.

Goals: Debt payments, savings, investments.

Fun: Dining out, entertainment, hobbies.

When you give every dollar a job, your income and your planned spending balance out to zero. There is no "leftover" money that’s vulnerable to mindless spending. You are in command.

How is it different from other budgets?

Traditional Budgeting: Often involves looking at past spending and adjusting slightly. It’s backward-looking and can justify past mistakes.

The 50/30/20 Rule: Suggests allocating income to needs, wants, and savings. It’s a good guideline but lacks the granular detail and intentionality of ZBB.

Zero-Based Budgeting: You build your budget from scratch ("zero") each month based on your upcoming income and goals. It’s proactive, detailed, and deeply intentional.

Why Zero-Based Budgeting is a Game-Changer for Beginners

Why put in the effort to budget this way? Because the rewards are transformative.

It Creates Total Awareness: You will know, down to the last dollar, where your money is flowing. This awareness alone can eliminate hundreds of dollars in wasted spending.

It Aligns Your Spending with Your Values: You get to decide what’s important to you. Want to prioritize travel over cable TV? A zero-based budget makes that choice explicit and actionable.

It Eliminates Guilt: When you plan for fun and spending money, you can enjoy it guilt-free. You’ve already ensured your bills and goals are covered.

It’s Incredibly Flexible: Life isn’t static, and neither is a zero-based budget. If your car needs a new tire, you can adjust your budget categories to accommodate it without derailing your entire month.

It’s a Powerful Communication Tool: For couples, a zero-based budget becomes a financial meeting agenda. It eliminates arguments about money because every dollar’s job has been agreed upon together.

A study by Ramsey Solutions found that 93% of people who use a zero-based budget say it works well for them, and it helps them reach their financial goals faster than any other method.

Before You Begin: What You Need to Get Started

Don’t worry; you don’t need anything fancy. Here’s your toolkit:

Your Income Figure: Know your exact take-home pay (your pay after taxes) for the month. If you have variable income, you’ll need to estimate conservatively.

Your Upcoming Bills: Gather your recurring bills (rent, car payment, insurance, subscriptions).

Your Spending History: Look at last month’s bank and credit card statements. This will help you estimate categories like groceries and gas.

A Tool to Budget With:

The Analog Method: A simple notebook and pen. Highly effective and tangible.

The Digital Method: A spreadsheet (Excel or Google Sheets). We’ve included a free template for you below.

Budgeting Apps: Apps like EveryDollar (Dave Ramsey’s app) are built specifically for this method and can link to your bank accounts to automate tracking.

The Step-by-Step Guide to Creating Your First Zero-Based Budget

Follow these steps at the end of one month to plan for the next.

Step 1: List Your Monthly Income

How much money will you actually receive next month? Include:

Primary paychecks (after tax)

Side hustle income

Expected bonuses or tips

Child support or other regular income

Variable Income Tip: If your income changes each month, use the amount from your lowest-earning month in the past 6 months as a conservative baseline. Any extra can be assigned as it comes in.

Total Monthly Income: $________

Step 2: List Your Monthly Expenses

This is the heart of the process. Go through your past statements and think about your upcoming month. Create budget categories for everything. Here’s a common list to get you started:

Essential Expenses (The Four Walls):

Giving/Charity

Savings (Emergency Fund, Sinking Funds)

Housing (Rent/Mortgage)

Utilities (Electric, Water, Gas, Internet)

Food (Groceries only)

Transportation (Gas, Public Transit, Car Payment)

Insurance (Health, Car, Renters)

Other Necessary Expenses:

Healthcare (Copays, Medications)

Personal (Basic toiletries, haircuts)

Debt Payments (Credit Cards, Student Loans beyond minimums)

Lifestyle Expenses:

Dining Out

Entertainment (Streaming, hobbies, movies)

Clothing

Fun Money (No-questions-asked cash for you and your partner)

Step 3: Assign a Job to Every Dollar

Now, the magic happens. Start subtracting your planned expenses from your income.

Begin with your essential expenses—the Four Walls. Then, move to your other necessities. Finally, assign money to your lifestyle and goals.

Your goal is to get to zero. If you have money left over after listing all your expenses, you haven’t finished the budget! Give that money a job. Do you need to add more to your emergency fund? Pay extra on a debt? Put it toward Christmas savings?

Example:

Income: $4,000

Expenses:

Rent: -$1,200

Groceries: -$400

Utilities: -$300

Gas: -$200

...and so on through all categories...

Final Category: Extra Debt Payment: -$150

Total Income – Total Expenses = $0

Step 4: Track Your Spending Throughout the Month

A budget is not a "set it and forget it" plan. It’s a living document. Throughout the month, track your transactions.

If you use cash, use the envelope system.

If you use a debit card, record every transaction in your notebook, spreadsheet, or budgeting app immediately.

This seems tedious at first, but it’s how you build awareness and stay accountable.

Step 5: Adjust as You Go

You will overspend in some categories. That’s okay! Life happens. This is the flexible part.

When you overspend in one category, you must cover it by underspending in another. If you spend $50 extra on dining out, you need to find $50 to move into that category. Maybe you decide to spend $50 less on entertainment this month.

This process of "rolling with the punches" is what makes zero-based budgeting sustainable. It doesn’t fail when you make a mistake; it teaches you to adapt.

Free Zero-Based Budget Template

To make it easy, here’s a simple template you can copy into Google Sheets or Excel.

Common Zero-Based Budgeting Mistakes (And How to Avoid Them)

Mistake 1: Forgetting Irregular Expenses. You will forget about annual insurance premiums or holiday gifts. Solution: Create sinking funds—small, monthly savings categories for these expenses.

Mistake 2: Not Budgeting for Fun. A too-strict budget will break you. Solution: Always include a "Fun Money" category to avoid burnout.

Mistake 3: Giving Up After One Month. Your first budget will be a guess. It will be wrong. Solution: Stick with it. It takes 3-4 months to get good at estimating your categories.

Mistake 4: Not Communicating with Your Partner. Solution: Have a monthly budget meeting. Make it a positive event to get on the same page.

For more on managing those pesky irregular costs, read our guide on essential sinking fund categories every budget needs.

Final Thoughts: Your Money, Your Control

Starting a zero-based budget is the single most powerful step you can take to change your financial trajectory. It moves you from a passive observer of your money to its active, intentional commander.

The first month will be clunky. The second month will be better. By the third month, you’ll start to feel a sense of control you’ve never experienced before. You’ll stop fearing unexpected bills because you’ve planned for them. You’ll watch your debt shrink and your savings grow because you’re telling your money to make it happen.

Your financial peace is waiting on the other side of a plan. That plan starts with a zero-based budget.

Your assignment: Before the next month begins, block out one hour. Grab your paycheck stubs and bills, and use the template above to create your first zero-based budget. Give every dollar a name. You’ve got this.

Ready to pair your new budget with a powerful debt-payoff strategy? Learn how the debt snowball method can help you eliminate your debts for good.

Comments